If you’re a holder of any OPI bond, you have an important vote coming up.

Here’s the situation: on October 31, 2025, Office Properties Income Trust filed for bankruptcy.

This is the court docket with all filings, you can search for Docket 26 which contains the petition detail:

Office Properties Income Trust Case Docket

You can also automatically download the Docket 26 pdf directly here:

Declaration in Support of Chapter 11 Petition

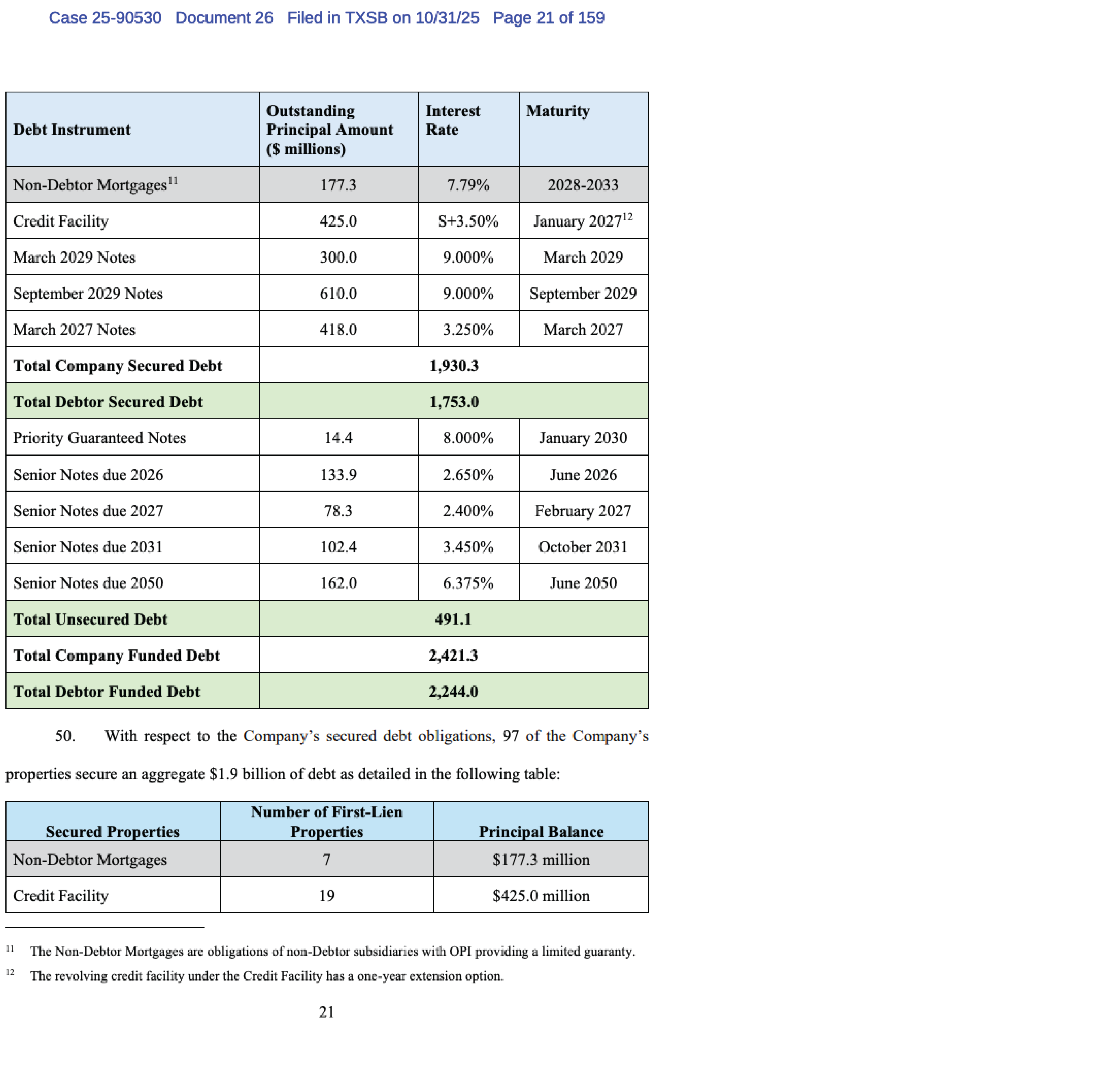

There are a few, though not many, important sections in Docket 26 and the first one is the Prepetition Capital Structure on page 21:

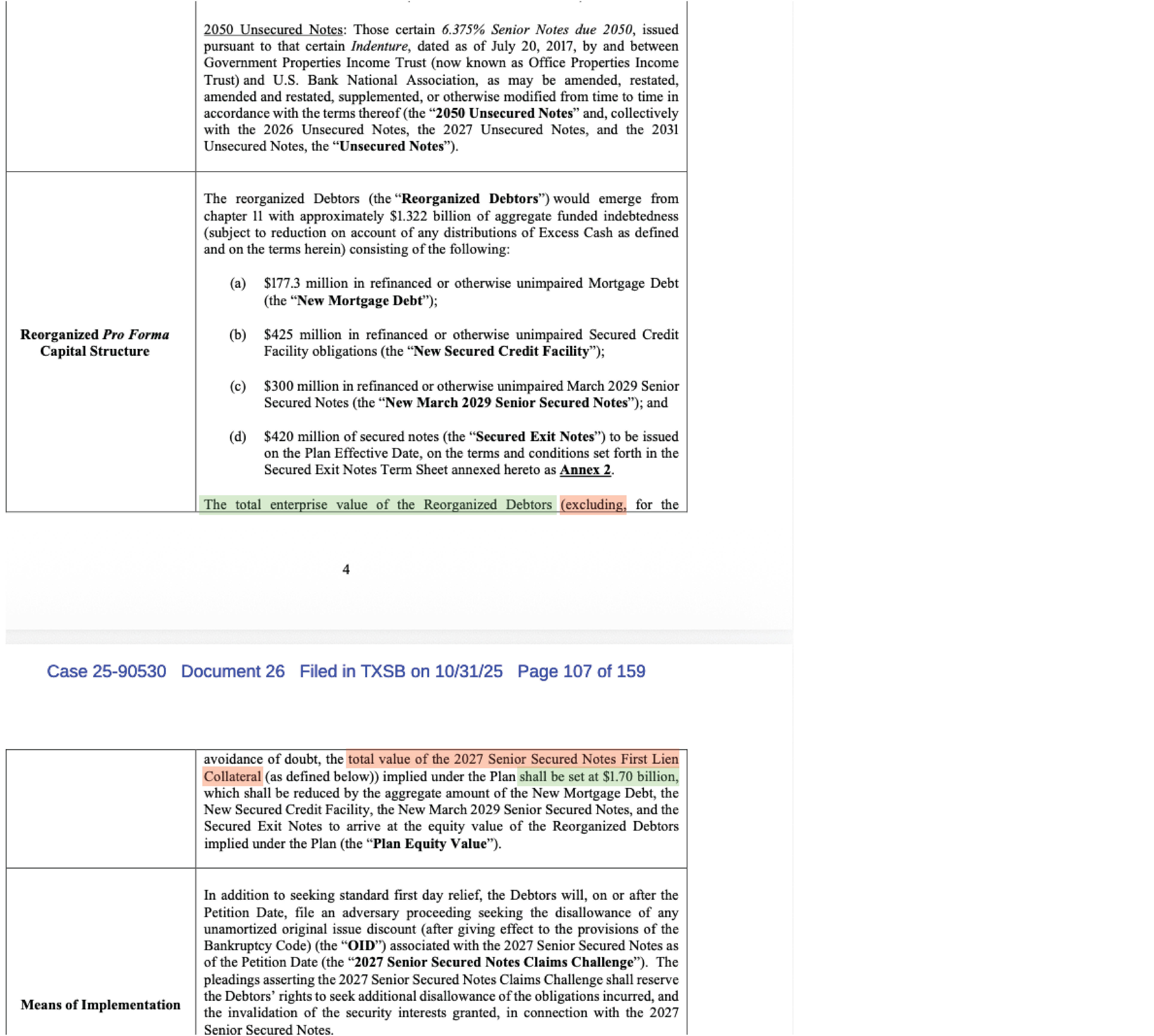

The second meaningful section is the enterprise value on pages 106-107 of Docket 26 (pages 4-5 of the Restructuring Term Sheet):

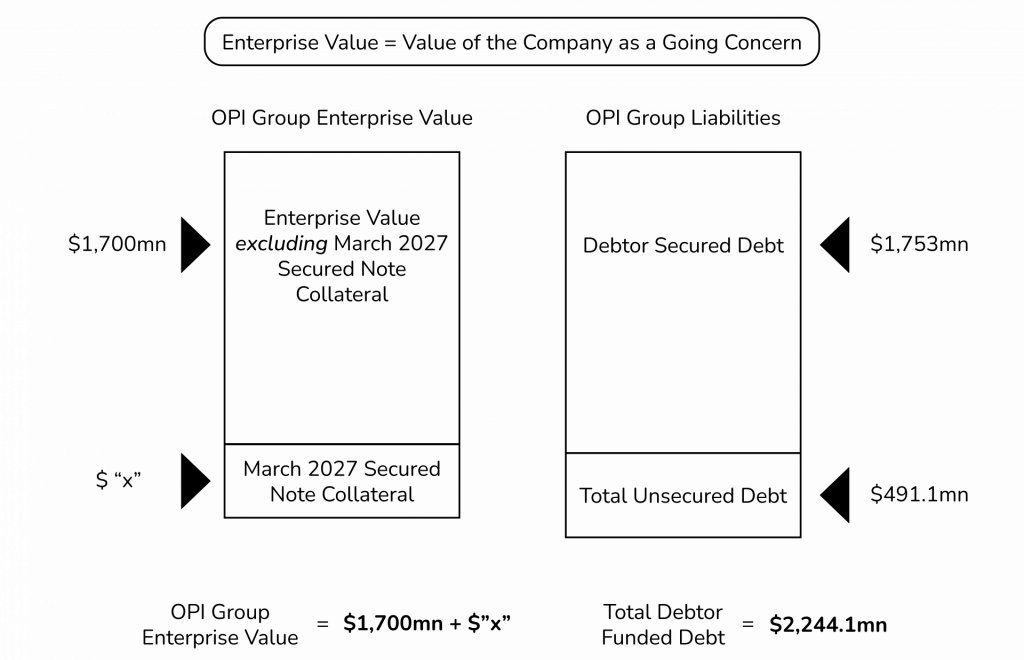

Let’s keep in mind a couple of things:

- The enterpise value of $1.7bn.

- The fact that it excludes the 2027 Senior Secured Notes First Lien Collateral while the Secured Debt section of the Prepetition Capital Structure above includes $418mm of outstanding principal for “March 2027 Notes.”

Here’s what we know so far:

Now let’s do a bit of algebra and see if we can figure out the value of “x,” the current market value of the March 2027 Secured Note Collateral.

The most recent property level detail is available from the company’s website, 2025 Q2 Earnings, Financial Results:

Here’s the PDF document:

Financial Results and Supplemental Information, Second Quarter 2025

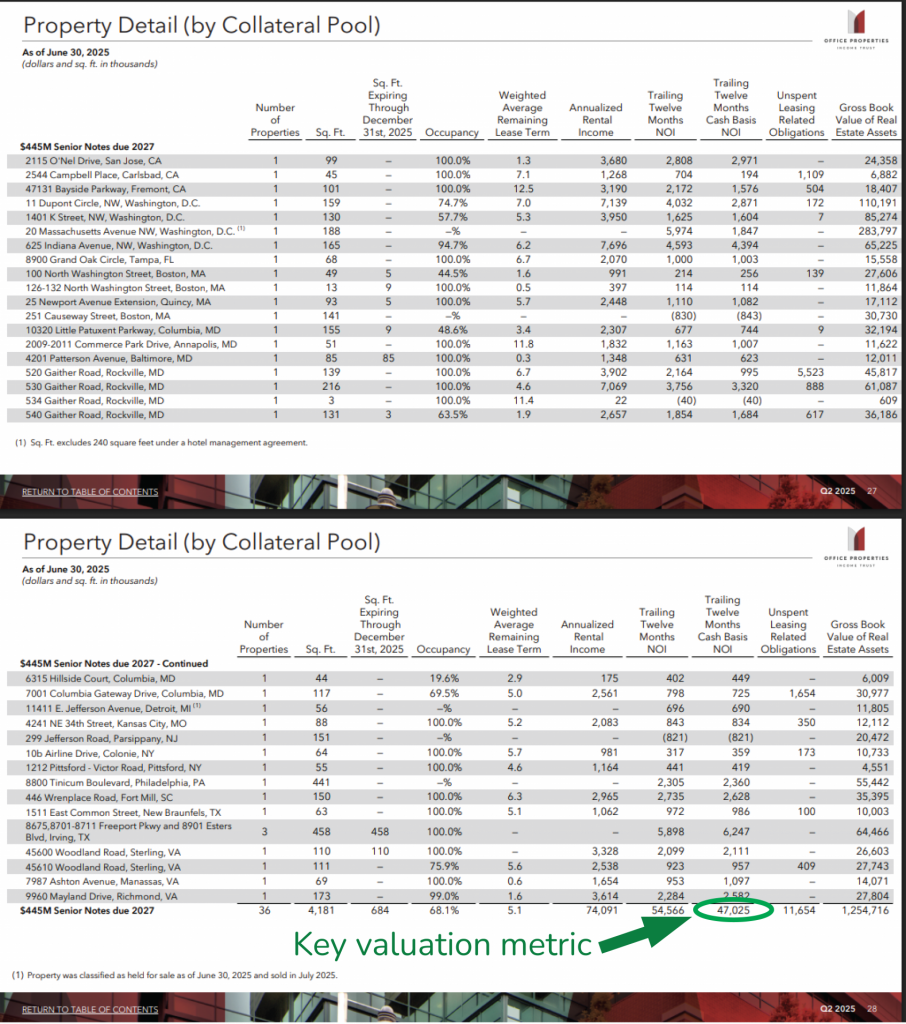

A list of March 2027 Secured Note Collateral starts on p27:

Cash Basis NOI (Net Operating Income) is the essentially the cash income produced by a property after cash operating expenses are paid.

Cash Basis NOI = Cash Rent Collected – Cash Operating Expenses

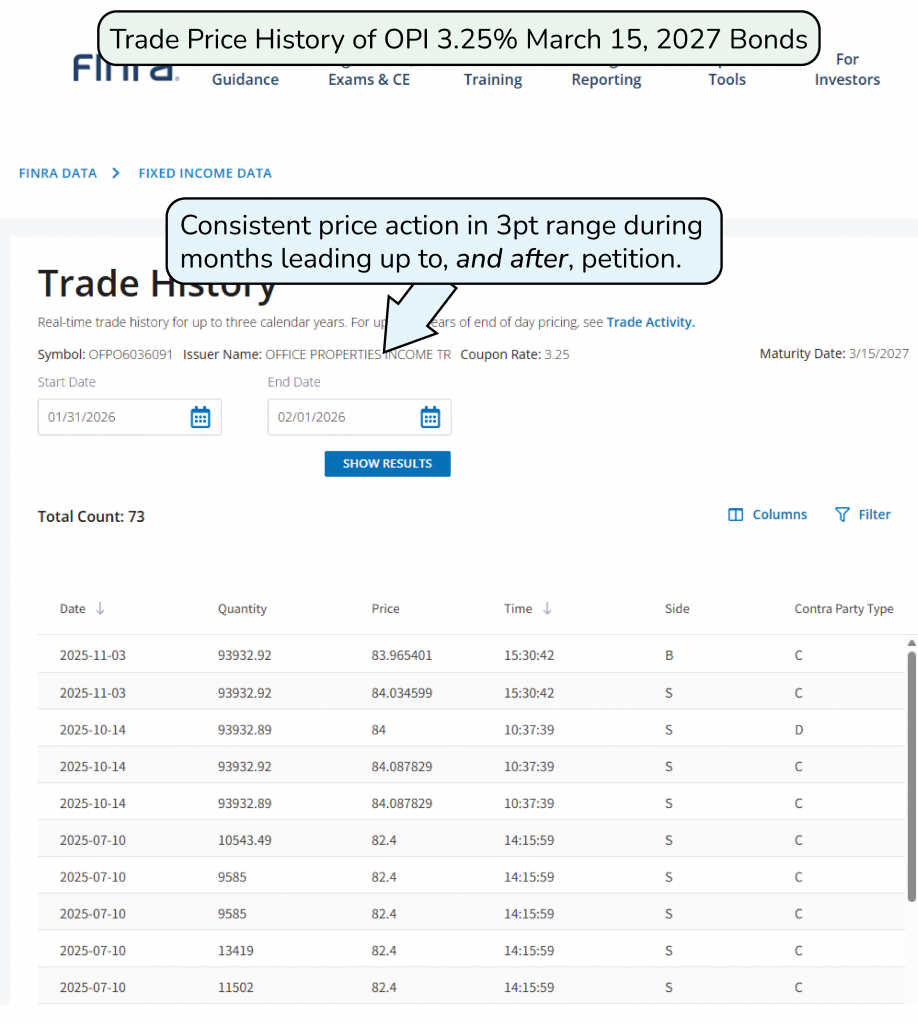

Now let’s look at where the market values the bonds that are backed by that collateral.

Fortunately, for that, we have a system called TRACE that publicly dislays the trade prices of bonds:

Here’s a link to view this information directly in the TRACE system: OPI 3.25% Mar 15 2027 TRACE

Allowing for a discount relative to the most recent traded levels, let’s assume a price of 83 for this bond.

The outstanding face amount is $418mm as we saw in the Prepetition Capital Structure above.

On this basis, the market value of the outstanding amount of the bond would be approximately $418mm x 83% = 347mm.

Of course, the most important caveat is that trade sizes were small, less than 1% of outstanding face.

Given that the issuer was widely expected to default for months before its petition, however, and the trade level was essentially unchanged after the petition, it’s hard to argue that the value in the bond represents any more than the underlying collateral.

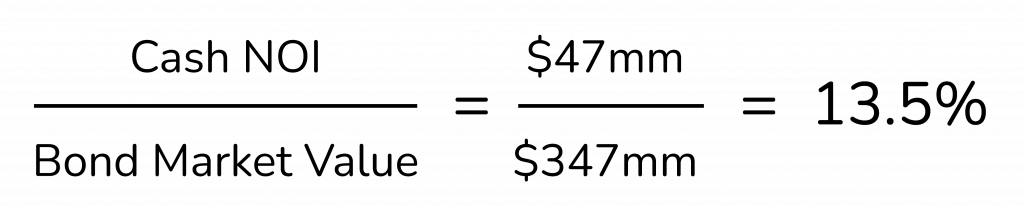

Let’s try one more valuation process.

If the value of the entire bond is $347mm, how does that compare to cash earnings, or cash NOI, of the collateral property?

If we agree that the bond value is equivalent to the Property Current Market Value then: